The Legal Case For Nullifying Debt Contracts and a Remedy for Damages Incurred by the Public

Notice

I am writing a legal case to nullify all debts denominated in US dollars on the basis of their fraudulent nature. This lawsuit will also be seeking compensation for real damages incurred by this fraud for myself and all those participating should this become a class action lawsuit. If you would like to participate as a plaintiff or on the legal team, you can email me at moorezt86@gmail.com. Please indicate the details of the debt contract you are disputing including the amount, the collateral (eg home, auto, etc), and the servicing institution.

I have also started an objections and answers post here: https://thinkingwithzach.blogspot.com/2023/10/objections-and-answers-lawsuit.html

If you have an objection that needs an answer, please write me at moorezt86@gmail.com and I’ll include it in the post

The Legal Case For Nullifying Debt Contracts and a Remedy for Damages Incurred by the Public

Introduction

In 2009, at age 71, Bernie Madoff, once one of the most renown hedge fund managers in the world, pleaded guilty to 11 federal felony counts, including securities fraud, wire fraud, mail fraud, perjury, and money laundering. The Ponzi scheme became a potent symbol of the culture of greed and dishonesty that, to critics, pervaded Wall Street in the run-up to the financial crisis. Madoff, the subject of numerous articles, books, movies, and biopic miniseries, was sentenced to 150 years in prison and ordered to forfeit $170 billion in assets, but no other prominent Wall Street figures faced legal ramifications in the wake of the crisis.

In this post, I shedding light on a much larger fraudulent enterprise that affects billions of people. I am speaking of the modern financial system that creates fraudulent money at the Federal Reserve through a unfair monopoly on money printing and at the local bank level through fraudulent fractional reserve banking.

The Questions I Have

- Is the definition and illegality of fraud well documented and enforced in the United States?

- Is the method of money creation without any real-asset backing it practiced by the Federal Reserve a fraudulent scheme?

- Is the method of money creation in the banking system, also known as fractional reserve banking, fraudulent?

- Have the Federal Reserve bank and the federal government colluded to ensure the damages incurred by the fraud inherent in the system are realized by the public through future taxation, not the banks?

- Are real and significant damages incurred by those who contract with these loan origination businesses?

- Are damages in this money creation scheme incurred to the degree a participant is removed from the originating source, making this fraud analogous to a standard pyramid scheme, which is illegal?

- Is the legality of loan contracts nullified by the fraudulent money creation practice used in the creation of these loans?

- Is it necessary that damages are remedied by guilty parties to the victims of this fraud in real assets, not U.S. dollars?

The definition, illegality, and enforcement of fraud is well documented and enforced in the United States of America.

The Method of Money Creation Practiced by the Central Banks is Fraudulent

Most people have heard that our currency is “printed out of thin air” and are vaguely aware of inflation as a threat to their savings.

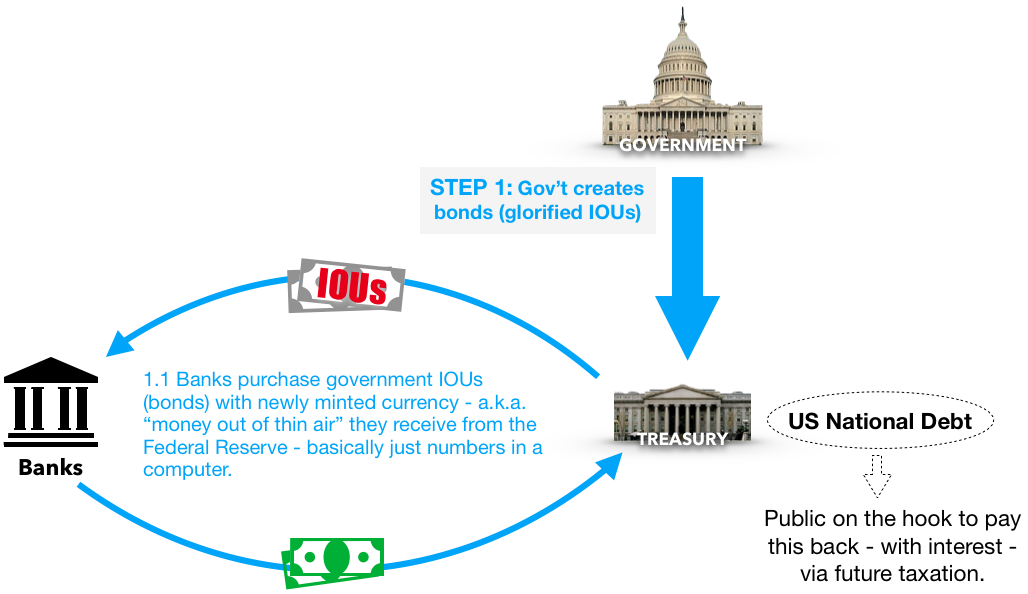

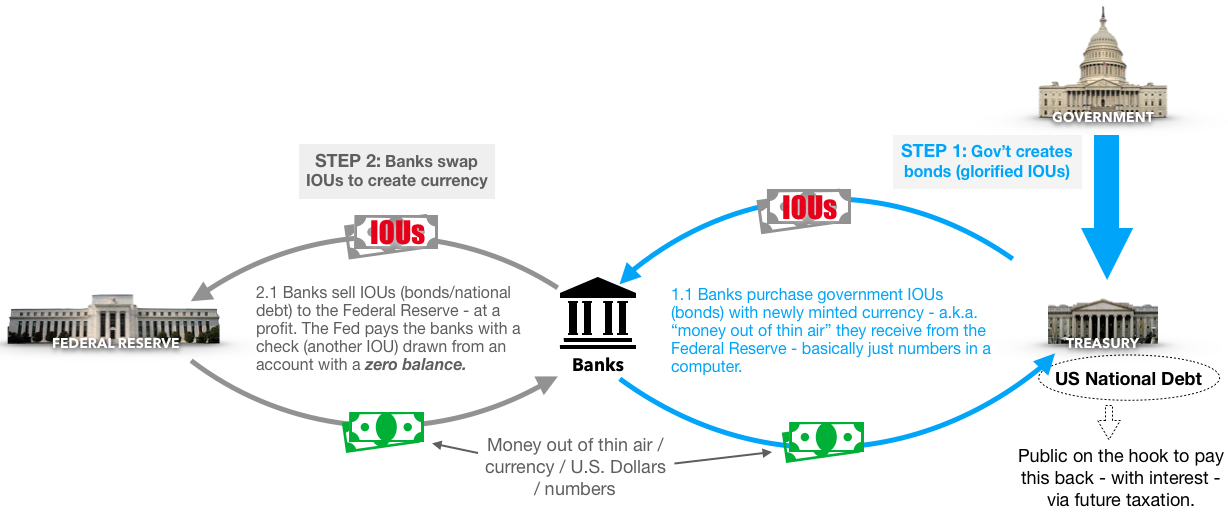

To create money, The U.S. Treasury issues a bond, essentially a promise (glorified IOU) that if you give us $100 today we’ll repay you that $100 plus interest at some set time in the future. These bonds / promises / glorified IOUs are called treasuries and are paid back via taxation.

Treasuries are sold at auction to the big banks (“primary dealers”), who either earn interest by holding the bond, or more typically re-sell these bonds to the Federal Reserve (the central bank of the United States).

The Federal Reserve (from hereon referred to as the Fed) purchases these bonds from the big banks at a guaranteed profit by writing the banks a check (another glorified IOU).

Now where did the Fed get the money to buy the government bond? Herein lies the fraud. The Fed simply creates dollars out of thin air. This means that all dollars are loaned into existence via the Federal Reserve. This monopoly the Federal Reserve has on debt-based money creation represents an unjust advantage over it’s customers which injures that person or entity, which makes this practice fraudulent.

The Fed has a bank account with no money in it, and they use that account to write a check to buy government issued debt from the primary dealers (big banks) who initially purchased them at auction from the Treasury.

To put this succinctly, here is an excerpt from the Boston Federal Reserve in 1984:

“When you or I write a check there must be sufficient funds in our account to cover the check, but when the Federal Reserve writes a check there is no bank deposit on which that check is drawn. When the Federal Reserve writes a check, it is creating money."—Putting It Simply, Federal Reserve Bank of Boston, 1984

This is money laundering and a fraudulent system. The money that comes into existence from the Fed cannot be paid back, because it is loaned at interest. In order for it to be paid back, new money must come into the system, which is a key feature of any pyramid or Ponzi scheme. The moment new money stops flowing into the system, the system collapses under the weight of its own fraud.

If you prefer a narrated video walkthrough, check out Chapter 8 of Peak Prosperity’s Crash Course below.

The method of money creation in the banking system, also known as fractional reserve banking, is fraudulent.

Your typical bank makes loans using what is called Fractional Reserve Banking. When you deposit money into the bank, banks are only required to hold a 10% reserve against that deposit. This means that if you deposit $100 into your account, the bank only has to keep 10% of that on hand (called vault cash, just in case you want some) – the other 90% it is free to loan out. The bank replaces the $90 it takes from your account with bank credit – another made up IOU.

The bank then loans out $90 of your initial $100 deposit. With this simple practice, there are now $190 in “existence” from an initial deposit of $100. The borrower will take the money lent to him, go and make a purchase (house, car, business investment etc.) and pay the seller with the $90 from your initial $100 deposit. The seller then deposits his $90 into a bank account, and that bank now loans out $81 (90%) of that deposit. There are now $271 in circulation.

And so on it goes, until ultimately a $100 cash deposit creates $1,000 in new, circulating currency.

The banking sector's use of fractional reserve lending is the primary engine of currency creation in modern fiat currency systems. It is estimated that 92-96% of all currency in circulation today is created by the banks, not the government. When a commercial bank loans an individual money, they create new deposit dollars in accounts on their books in exchange for a borrowers IOU. Said more simply, when you go get a loan from a bank to make a purchase, they literally type numbers into your account (and you have to pay back those made up numbers with interest).

The bank, by treating both the deposit and the loan as an asset, is engaging in fraud. If all depositors were to pull their money out of the bank, 90% of the money would be found missing. It is only the shear volume and complexity of the system that prevents people from seeing this fraud.

To make this point clear, let’s say you are a rancher living in a small town of three people, including you, a farmer, and a banker. You and the farmer each deposit $100,000 into the bank available for withdraw on demand. Upon deposit, the banker loans the farmer and the rancher $90,000 each. There is now $380,000 in the system from just $200,000 in deposits. If the farmer and the rancher immediately paid off their loans using their original deposits, the small town would have one ranch, one farm, and $20,000 in it, with the bank making off with $180,000! Therefore, through fractional reserve banking, the banker has stolen 90% of the farmer’s and rancher’s purchasing power. In addition, because loans are paid off over time and with interest, it would not be long before the total liability of the $180,000 in loans exceeded the original $200,000 in deposits. Simple math will then dictate that it is impossible for the full amount of the loan with interest to be paid back, resulting in a foreclosure. When this happens, the bank will claim the farm and the ranch as collateral on the loan, leaving both the rancher and the farmer with neither money nor real-estate.

This simple illustration is played out on a large scale across the entire US economy, with banks stealing purchasing power through fractional reserve lending and claiming real assets as collateral when the impossible to repay loans go into foreclosure.

This is perhaps why Henry Ford who was 50 years old when The Federal Reserve was created, said this about the modern banking system:

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

The Federal Reserve bank and the federal government have colluded to ensure the damages incurred by the fraud inherent in the system are realized by the public, not the banks.

The Treasury established several programs under TARP (Troubled Asset Relief Program) to help stabilize the U.S. financial system, restart economic growth, and prevent avoidable foreclosures.

Although Congress initially authorized $700 billion for TARP in October 2008, that authority was reduced to $475 billion by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). Of that, the following amounts were committed through TARP's five program areas:

- Approximately $250 billion was committed in programs to stabilize banking institutions ($5 billion of which was ultimately cancelled).

- Approximately $27 billion was committed through programs to restart credit markets.

- Approximately $82 billion was committed to stabilize the U.S. auto industry ($2 billion of which was ultimately cancelled).

- Approximately $70 billion was committed to stabilize American International Group (AIG) ($2 billion of which was ultimately cancelled).

- Approximately $46 billion was committed for programs to help struggling families avoid foreclosure, with these expenditures being made over time.

Real and significant damages are incurred by those who contract with these loan origination businesses.

In this money creation scheme, damages are incurred to the degree a participant is removed from the originating source, making this fraud analogous to a standard pyramid scheme.

The legality of loan contracts is nullified by the fraudulent money creation practiced used in the creation of these loans.

It is necessary that damages are remedied by guilty parties to the victims of this fraud in real assets, not US dollars.

Conclusion

“Gentlemen, I have had men watching you for a long time and I am convinced that you have used the funds of the bank to speculate in the breadstuffs of the country. When you won, you divided the profits amongst you, and when you lost, you charged it to the bank. You tell me that if I take the deposits from the bank and annul its charter, I shall ruin ten thousand families. That may be true, gentlemen, but that is your sin! Should I let you go on, you will ruin fifty thousand families, and that would be my sin! You are a den of vipers and thieves." - Andrew Jackson (US President 1829-1837)

Notes on Contributing to the Movement:

I will make notes of monetary and non-monetary provisions needed below as the case and movement gains momentum. In the meantime, what we need is for this to be shared and advocated for. The more people know about this, the more likely it will succeed.

If you’d like to join this movement either as a plaintiff or on the legal team, please reach out to me at moorezt86@gmail.com.

If you’d like to contribute to this movement monetarily, you can make contributions in the following ways.

Venmo: @zach-moore-8

Bitcoin: My Public Address to Receive BTC: bc1qrr8akh5dhtd70kht83kmtzpgzfdmsdgwzxufeh

|

| Simply scan this QR code to contribute Bitcoin |

For a future worth inheriting,

Zach Moore

Comments

Post a Comment